Perspectives on the global economic changes

Re: Perspectives on the global economic changes

well Karl max pointed that currrncy is just a tool to trade "human effort" 150 years ago, which is taught in Chinese mid school for decades.......allmost all chinese know it.

Re: Perspectives on the global economic changes

Superbly put. This is the best and simplest way to explain it. Great.narendranaik wrote: That's a nice ideological speech but doesn't aid the current debate being flaunted by some here. Gold (and silver and other precious metals)

are the real currency and are definitely more credible than paper. Paper doesn't has any value when it is not backed by anything. It's like saying a house contract is "real" but the house with which it is backed is not.

When in reality the contract is merely a representation that the house actually belongs to it's owners. Without the house, the contract is as good as a toilet paper. You can print/xerox countless contracts, but without the house, they are meaningless. Paper currency is similar to the contract.

I think you are wrong. You are confusing cause and effect. Gold is not valuable because its difficult to extract. On the other hand, gold is mined and extracted because it is seen as valuable.Vriksh wrote: Why is gold so valuable... is it because it is shiny or because we use it to measure human effort. The answer is the latter 1) Back in the day it used to take 100 mandays to extract and deploy 1g of gold and therefore if someone owned 1 g of gold he/she could trade it for 100 mandays of work say like building a house.

So, basically, something needs to be seen as intrinsically valuable. If it is valuable, then it can be used to trade with something else that is valuable.

Services(i.e. manhours) are just one such valuable entities. There are other things in nature which are intrisically valuable. For example, oil is valuable intrisically because it has the ability to burn as fuel.

Since, it is valuable, people will invest manhours to extract and mine it. So, you have to understand that first an object needs to be seen as valuable for people to invest in it. Object doesn't become valuable because people invest money in it.

It does not matter whether there is effort(human or otherwise) or not. What matters is whether someone perceives it as valuable/useful or not.Vriksh wrote:So really speaking we are now simply using various currencies/gold to measure and trade human effort. USA has created tremendous value over the last 200 years it is visible in the freeways, the cities and the universities that exist out there, so has China and many other nations. Indian human effort measured as gold was shipped out the country for nearly free during British times and we are poor today since the reserves of human effort we had built up was destroyed.

If you have something which I see as valuable, then you can trade it with something that I have which you see as valuable. As simple as that. No need to complicate it.

First question is: useful to whom?

Obviously, human beings. Directly or indirectly, its human beings which need to find it valuable.

Second question: what are the basic needs of human beings?

Food, sleep, rest, work, play, mating, child-care, health-care, and protection/security.

At civilization level, the humanity needs: clothes, state machinery, farming, hospitals, roads, temples, schools, ships/boats, ports, ...etc.

In modern economy, electronic goods and mechanical instruments play a major role.

This applies to any object which is seen as valuable. If its supply exceeds demand tremendously, then its value will drop. BTW, thats exactly what is happening with fiat currency. The govts and banks keep printing them so much that its value keep dropping. That means inflation.The day we find a way to manufacture gold (looks extremely difficult) then its value will automatically drop in terms of mandays required. This was essentially what Adam Smith propounds. The legitimate question is what happens when we have excess amount of human effort available. At that time we will not be able to deploy the human labor to create value and very likely the excess labor will consume what has already been builtup.

Gold or silver or other such precious metals cannot be printed on a whim. If someone finds a way to print large quantities of Gold or silver or other such precious metals, then they too will not be useful as currencies.

Only gold as a currency will not be a good system because some powerful entities will try to hoard the gold and capture the market. So, gold has to be supplemented with silver. Then, it becomes very difficult for anyone to capture the market.

The coins(i.e. currency) historically is an attempt to do this. Gold and silver are used to create coins. Each coin will have unique combination of gold and silver thus it represents different denominations.

Fiat currency is just paper which claims that a person can get money in future. What is that money?

For example, every rupee note carries a promise: "I promise to pay the bearer a sum of x rupees". What are these rupees? Why would a person carrying a rupee note be promised to pay rupees? That means the rupee note is not the real rupee. The real rupaiya was made up of a silver. Silver coins used to be the rupaiya. The rupee note was introduced as a go between. It was a sort of a promise to pay the real rupaiya in future.

I think there are so many contradictions in what you are saying and it reflects the contradictions of economy based on fiat currency.chola wrote:We desis love gold which is why we want to believe that gold is the only real currency.

The truth is if the world were on a pure gold standard, the world would never have a middle class or a modern economy for that matter.

As an Indian, we should pray that gold does not become a standard or else India stays poor for eternity.

A modern economy creates wealth by the goods and wealth it can produce not by the amount of gold it can dig out of the ground.

If goods and 'wealth'(what is wealth?) can be created easily and cheaply by modern tech, then those goods and 'wealth' would be cheap.

If goods and 'wealth' can be created with a lot of cost, then they will be costly.

Its as simple as that.

But fiat currency is introducing a new angle into this: inflation and debt.

Fiat currency allows some people to keep printing whenever they feel like.

Fractional banking allows some people to give more loans than they have money for.

To use Narendra Naik ji's analogy: If I say that I want to lease more houses than I own, will anyone accept it? If I produce house documents of 100 houses, but have only 1 house on ground, then will people allow me to lease 100 houses to 100 people?

No. Because, on ground, there is only one house. So, I can only lease one house.

When banks try to loan more than they have, they are fooling people. Giving fancy names to this deception is only meant to make people fools.

So, what is happening is that a debt based economy with constant inflation has been created. It is unsustainable.

The only solution seems to be to return to basics.

What are the basics of economics?

Simple.

Buy, sell, profit/loss, debt/loan, loaned to/indebted to, future potential.

Future potential is a perception by others and is necessary to assess whether the loans or debts will be cleared or not. If the future potential is positive, then the people who loaned the money will not pester for immediate clearance. If the future potential is negative, then the people who loaned the money will pester for immediate clearance i.e. bank run. The problem for banks is that they loan much more than they own. So, whenever all people ask for money, they don't have enough.

This is just bad banking.

The first step is to eliminate fractional banking. You can only loan what you own. If you are a bank, then you can loan what others save with you, but you cannot loan more than that. Even this is a risky business. But, its far better than the present situation where banks loan much more than anyone saves with them.

Banks simply create money out of thin air by giving loans. This causes inflation.

The second step is to eliminate fiat currency and find some other material as the currency. That other material has to be intrinsically valuable and cannot be created on a large scale on a whim.

That means, dollar has to be replaced or bypassed.

China is hoarding gold because it has understood that hoarding dollars is just useless. America can keep printing those dollars.

When India stop import of gold, they are doing something that terrible in the long run. Because, they are stopping people from owning gold. On the other hand, china and central banks own stashes of gold.

What you are essentially saying is that modern economy is not possible without the cheap debts. That means most of the modern western economy is based on cheap debts. And most of these debts are created out of thin air i.e. people/banks who are giving debts themselves don't own. They giving out more than they own. This is simply cooking books.

So, this modern western economy is just cooking books to appear as rich when in reality they don't have the funds to invest in all those public sector buildings in which they invested so heavily.

For example, when a road is built: is that road intrinsically valuable. It is not valuable to build a road unless the road can generate more income than its building will cost.

So, building infrastructure in itself is not something of value unless that infrastructure can directly or indirectly give more returns to the economy.

In Bhaarath, due to geography and population, building infrastructure is mostly valuable. This is not true in rest of the world. Unless geography and populations can support, building infrastructure is a pure luxury in many places around the world.

Bhaarath has a huge coast line and large amount of raw resources including human resource. So, it needs infrastructure to manage this geography and population. So, Bhaarath's case infrastructure is a necessity. On the other hand, for rest of the world, infrastructure is a luxury.

Most of the world, did not have great infrastructure unless they were an imperial kingdom. Only in Bhaarath, infrastructure is a necessity. Maybe south china is another place where infrastructure is a necessity. Infrastructure in Tibet or north-china is a luxury.

If luxuries are bought using debts, then its a bad model. Necessities can be fulfilled using debts. But, luxuries should not be funded using debts.

Today, western economies have only thing which they can trade: Knowledge or technology.

Interestingly, they don't want to trade this. Because they know that others can soon learn it themselves and surpass them. So, they create restrictions on transfer of technology.

What they instead are doing is: they are using other countries to build valuable objects using their technology and then sell the objects. This is a circuitous route to avoid the transfer of technology.

For example, American companies are manufacturing in China and then selling those objects all over the world.

But, sooner or later, those who are manufacturing will learn the technology and start competing. This is also happening. The chinese are starting to manufacture and starting to compete with American companies.

Now, once the Chinese have learnt the basic technology, then it becomes really difficult for the American companies. Because how long can they sustain their dominance with superior technology? How long will it take for the Chinese to manufacture the same technology as Americans?

It may take a decade or a two.(Conservative estimate). But, soon, the American or westerners will lose that technical superiority also. Then, what? Then, what will the western economies sell or export?

In the long run, western economies cannot sustain their current levels of infrastructure or public spending.

Bhaarath and China are the only ones who can gain on this because they are the largest countries in terms of population.

So, the western economies have to keep inventing new technologies if they have to maintain their superiority. Bhaarath and China will become superior even if they match the technology of west. Bhaarath and China don't need to invent new technologies. They need infrastructure to manage the populations. They need to create jobs to productively engage the populations.

Re: Perspectives on the global economic changes

The real legal tender is 1 Rupee coin/note (at present notes are withdrawn). So RBI, is not owner, but just issuer, so it contains promise to pay (its an obligation, because the real Rupee is issued is GoI). That is why 1 Re note is signed by finance secretary, but not by RBI governor.johneeG wrote:For example, every rupee note carries a promise: "I promise to pay the bearer a sum of x rupees". What are these rupees? Why would a person carrying a rupee note be promised to pay rupees? That means the rupee note is not the real rupee. The real rupaiya was made up of a silver. Silver coins used to be the rupaiya. The rupee note was introduced as a go between. It was a sort of a promise to pay the real rupaiya in future.

For more details, please go through the RBI link, which explains it.

http://www.rbi.org.in/scripts/BS_Curren ... aspx?Id=39

Re: Perspectives on the global economic changes

All banks do loan out only their own reserves or what others (individuals or entities) have lent them - in other words, what banks loan out (their assets) are always matched by corresponding liabilities (funds that other entities have saved with the bank). The only systemic issue with the banking system today is that of asset-liablity maturity mismatch.johneeG wrote:The first step is to eliminate fractional banking. You can only loan what you own. If you are a bank, then you can loan what others save with you, but you cannot loan more than that.

Re: Perspectives on the global economic changes

Putin: State Deficit Not to Grow, to Be Held at Controlled Level of Less Than 15% GDP

Any reason why they would maintain a low Public debt of 15 % ( current debt is 11 % of GDP ) in absence of external financing ? Ideally they would increast Public Debt to say 25 % of GDP via some sort of QE.

What good a low Public Debt would serve when most EU countries have debt of ~ 90 % of GDP and even BRICS average Public Debt is around ~ 50 %

BEIJING, November 10 (RIA Novosti) - Russia will not increase its state deficit and will hold it at a controllable level of no less than 15 percent of the gross domestic product, Russian President Vladimir Putin said Monday.

“There will be no growth in the state deficit. We plan on holding it at a safe controlled level of no less than 15 percent of the GDP,” Putin said during his speech at the Asia-Pacific Economic Cooperation summit in China.

Any reason why they would maintain a low Public debt of 15 % ( current debt is 11 % of GDP ) in absence of external financing ? Ideally they would increast Public Debt to say 25 % of GDP via some sort of QE.

What good a low Public Debt would serve when most EU countries have debt of ~ 90 % of GDP and even BRICS average Public Debt is around ~ 50 %

Re: Perspectives on the global economic changes

Xi Dangles $1.25 Trillion as China Counters U.S. Refocus

President Xi Jinping sought to counter U.S. efforts aimed at boosting influence in Asia by flexing China’s economic muscle days before a Beijing summit with his counterpart Barack Obama.

Speaking to executives at a CEO gathering in Beijing, Xi outlined how much the world stands to gain from a rising China. He said outbound investment will total $1.25 trillion over the next 10 years, 500 million Chinese tourists will go abroad, and the government will spend $40 billion to revive the ancient Silk Road trade route between Asia and Europe.

“China’s development will generate huge opportunities and benefits and hold lasting and infinite promise,” Xi said. “As China’s overall national strength grows, China will be both capable and willing to provide more public goods for the Asia Pacific and the world.”

Re: Perspectives on the global economic changes

Deep Divisions Emerge over ECB Quantitative Easing Plans

By Anne Seith

To prevent dangerous deflation, the ECB is discussing a massive program to purchase government bonds. Monetary watchdogs are divided over the measure, with some alleging that central bankers are being held hostage by politicians.

By Anne Seith

To prevent dangerous deflation, the ECB is discussing a massive program to purchase government bonds. Monetary watchdogs are divided over the measure, with some alleging that central bankers are being held hostage by politicians.

At first glance, there's little evidence of the sensitive deals being hammered out in the Market Operations department of Germany's central bank, the Bundesbank. The open-plan office on the fifth floor of its headquarters building, where about a dozen employees are staring at their computer screens, is reminiscent of the simple set for the TV series "The Office". There are white file cabinets and desks with wooden edges, there is a poster on the wall of football team Bayern Munich, and some prankster has attached a pink rubber pig to the ceiling by its feet.

The only hint that these employees are sometimes moving billions of euros with the click of a mouse is the security door that restricts access to the room. They trade in foreign currencies and bonds, an activity they used to perform primarily for the German government or public pension funds. Now they also often do it for the European Central Bank (ECB) and its so-called "unconventional measures."

Those measures seem to be coming on an almost monthly basis these days. First, there were the ultra low-interest rates, followed by new four-year loans for banks and the ECB's buying program for bonds and asset backed securities -- measures that are intended to make it easier for banks to lend money. As one Bundesbank trader puts it, they now have "a lot more to do."

A Heated Dispute

Ironically, his boss, Bundesbank President Jens Weidmann, is opposed to most of these costly programs. They're the reason he and ECB President Mario Draghi are now completely at odds. Even with the latest approved measures not even implemented in full yet, experts at the ECB headquarters a few kilometers away are already devising the next monetary policy experiment: a large-scale bond buying program known among central bankers as quantitative easing.

The aim of the program is to push up the rate of inflation, which, at 0.4 percent, is currently well below the target rate of close to 2 percent. Central bankers will discuss the problem again this week.

It is a fundamental dispute that is becoming increasingly heated. Some view bond purchases as unavoidable, as the euro zone could otherwise slide into dangerous deflation, in which prices steadily decline and both households and businesses cut back their spending. Others warn against a violation of the ECB principle, which prohibits funding government debt by printing money.

Is it important that the ECB adhere to tried-and-true principles in the crisis, as Weidmann argues? Or can it resort to unusual measures in an emergency situation, as Draghi is demanding?

A Mixed Record in Japan and the US

The key issues are the wording of the European treaties, the deep divide in the ECB Governing Council and, not least, the question of what monetary policy can achieve in a crisis. Is a massive bond-buying program the right tool to inject new vitality into the economy? Or does it turn central bankers into the accomplices of politicians unwilling to institute reforms?

The question has been on the minds of monetary watchdogs and politicians since the 1990s, when a German economist working in Tokyo invented the term "quantitative easing." Its purpose was to help former economic miracle Japan pull itself out of crisis after a market crash.

The core idea behind the concept is still the same today: When a central bank has used up its classic toolbox and has reduced the prime rate to almost zero, it has to resort to other methods to stimulate the economy. To inject more money into the economy, it can buy debt from banks or bonds from companies and the government.

The Bank of Japan finally began to implement the concept, between 2001 and 2006, but the country sank into years of deflation nonetheless. After the financial crisis erupted, central bankers in Tokyo tried a second time to acquire government bonds on a large scale, in the hope that earlier programs had simply not been sufficiently forceful. Between 2011 and 2012, the central bank launched emergency bond-buying programs worth €900 billion ($1.125 trillion). Finally, in 2013, the new prime minister, Shinzo Abe, opened up the money supply completely when he had the central bank announce a virtually unlimited bond buying program.

A Higher Debt-to-GDP Ratio than Greece

But the strategy, known as "Abenomics," worked only briefly. After a high in 2013, in which Abe proudly proclaimed that Japan was "back," industrial production declined once again. With a debt-to-GDP ratio of 240 percent, much higher than that of Greece, investments declined again, despite the flood of money released under Abenomics.

Businesses and private households were simply too far in debt to borrow even more, no matter how cheap the monetary watchdogs had made it. The banks, for their part, still failed to purge all bad loans from their books, because the central bank was keeping them artificially afloat. "For decades, the Japanese government did not institute the necessary structural reforms," says Michael Heise, chief economist at German insurance giant Allianz.

Ben Bernanke, the former chairman of the US Federal Reserve, demonstrated that under different circumstances quantitative easing could indeed work. After the collapse of investment bank Lehman Brothers, Bernanke, a monetary theorist, spent close to $1.5 trillion to buy up mortgage loans, corporate bonds and US Treasury bonds.

A second program was launched in 2010, followed by a third in 2012. This time the Fed decided that the program would continue until unemployment had declined to 7 percent. Bernanke's successor, Janet Yellen, only put an end to the latest round of quantitative easing last week.

During this period, the Fed, through its emergency measures, has inflated its balance sheet by about $1 trillion to $4.5 trillion, and the economy is now falling into step once again. Unemployment has dropped from 10 to 6 percent, and the annualized growth rate in the third quarter was 3.5 percent. Many observers believe that this alone proves that Bernanke's mega-experiment was a success.

Relatively strong consensus only exists over the fact that the Fed, with its massive intervention, quickly returned many credit markets to normality after the crisis erupted by buying up securities that suddenly no one else wanted. But have the quantitative easing programs also stimulated the economy in the long term?

In a study, the Fed itself concludes that its programs reduced the unemployment rate by 1.5 percent in 2012. Other studies found that long-term interest rates on government and corporate bonds declined significantly as a result of the Fed's buying spree. Still others question the efficacy of the programs, especially more recently.

So who's right? "It's nearly impossible to measure that," says Clemens Fuest, president of the Center for European Economic Research, "if only because we don't know what would have happened without the programs."

Strong Side Effects

The lack of certainty has led many economists to believe that the effects of the bond buying programs were not all positive. On the contrary, the longer the central bank pumps up the markets with its injections of liquidity, they warn, the stronger the policy's side effects get. Because yields on many investments declined along with borrowing rates, more and more market players ignored the risks associated with many halfway lucrative business opportunities.

In Europe, for example, bond traders and other investors began buying up Greek, Spanish and Italian government bonds after the debt crisis had subsided, so that some of the former crisis-ridden countries are now paying even lower interest rates on new borrowing than before. Meanwhile, in the United States, corporate debt securities known as junk bonds became the latest trendy investment.

Junk bonds come with an enormous risk of default, but they are also considered very high-yield investments. The market blossomed, at least until recently. But what this means for the US economy may not become apparent for several years. More than $700 billion in junk bonds will mature by 2018, and "a large number of companies will suddenly have great trouble finding follow-up financing," warns Allianz economist Heise.

On the global exchanges, the mood among investors was long delirious. In June, the Bank for International Settlements, an international organization of central banks, noted a "puzzling disconnect" between the boom and actual economic developments. Because debt has also been growing worldwide, the financial system is, in a certain sense, even more fragile than before the crisis, said Jaime Caruana, the bank's general manager.

Whether this is true could become apparent in the next few weeks. Once the Fed has stopped its ongoing injection of liquidity into the economy, many observers fear severe withdrawal symptoms in markets and exchanges.

Growing Pressure for ECB President to Act

Nevertheless, ECB President Draghi is coming under growing pressure to hazard the risky experiment in the euro zone. The region's economy is stagnating and inflation continues to decline. "If the central bank did nothing to counteract the threat of deflation, it would be like withholding treatment from a patient with pneumonia because of the potential side effects," argues Joachim Fels, chief economist with investment bank Morgan Stanley.

The only problem is that the recipe for cheap money is no longer showing much effect in Europe today. In September, ECB President Draghi offered banks four-year loans at ultra-low interest rates, under the condition that the institutions would pass on the funds to the economy through lending. But the amount of borrowing that ensued -- €82.6 billion -- was significantly less than anticipated.

The demand for credit is simply too low in many places. The economy is ailing as a result of a lack of investment and low consumption rates, because households and businesses in a number of countries are still in too much debt. Countries like Italy and France are also dragging their feet with important reforms that could make their industries competitive once again.

A 'Largely Pointless Exercise'

If the ECB does launch a buying program for government bonds, another problem arises. To avoid coming under the suspicion of trying to provide funding primarily to crisis-ridden nations, it will probably have to acquire the bonds of all euro-zone countries. For the ECB itself, the most likely approach is to simply base its bond-buying program on each country's initial contribution to the ECB, known as the capital key.

But then the central bankers would also have to buy large numbers of German bonds, which would be a "largely pointless exercise," as Willem Buiter, the chief economist at US bank Citigroup, puts it. Interest rates on some German government bonds are already in the negative range.

Buiter can readily be described as a proponent of active monetary policy, and yet he too believes that this approach only works if accompanied by structural reforms. Monetary policy alone isn't enough to combat persistent stagnation, he says, "which is what the euro zone is heading for."

It's no surprise that the ranks of skeptics are also growing within the ECB. Bundesbank President Weidmann has long warned that the central bank cannot be allowed to become a "sweeper" for policymakers. Now German ECB Supervisory Board member Sabine Lautenschläger is coming to his defense, saying that the purchase of government bonds could only be a "last resort" in the event of a deflationary spiral, essentially the final ammunition of monetary policy. The critics of further quantitative easing measures also include the Executive Board members from Luxembourg, Austria, the Netherlands and Estonia.

It was US economist Melvyn Krauss who proposed a compromise in the German financial newspaper Handelsblatt last week that many central bankers read with interest. According to Krauss, the ECB could exclude from a bond purchasing program countries that Brussels had admonished for deficit violations. In this way, quantitative easing would become an "enticement" for politicians to institute reforms.

Will Krauss's proposal produce a consensus? Europe's central bankers remain skeptical. "I don't see the south accepting this," one of them said, referencing to Southern European countries.

Re: Perspectives on the global economic changes

The market should decide interest rates, not some jokers sitting up in an ivory tower.

Meddling around with price fixing (i.e. interest rate "setting") and counterfeiting (i.e. money printing) is what destroys the productive economy. It also gives rise to the useless middleman banking parasitic economy which begins to then grow like a cancer.

Meddling around with price fixing (i.e. interest rate "setting") and counterfeiting (i.e. money printing) is what destroys the productive economy. It also gives rise to the useless middleman banking parasitic economy which begins to then grow like a cancer.

-

panduranghari

- BRF Oldie

- Posts: 3781

- Joined: 11 Aug 2016 06:14

Re: Perspectives on the global economic changes

I said it before and I say again - ECB wont do QE as the Marjolin Memorandum and Maastricht treaty does not allow that.Austin wrote:

Growing Pressure for ECB President to Act

Nevertheless, ECB President Draghi is coming under growing pressure to hazard the risky experiment in the euro zone. The region's economy is stagnating and inflation continues to decline. "If the central bank did nothing to counteract the threat of deflation, it would be like withholding treatment from a patient with pneumonia because of the potential side effects," argues Joachim Fels, chief economist with investment bank Morgan Stanley.

There is a last resort option for ECB. They will devalue Euro against dollar.Austin wrote: It's no surprise that the ranks of skeptics are also growing within the ECB. Bundesbank President Weidmann has long warned that the central bank cannot be allowed to become a "sweeper" for policymakers. Now German ECB Supervisory Board member Sabine Lautenschläger is coming to his defense, saying that the purchase of government bonds could only be a "last resort" in the event of a deflationary spiral, essentially the final ammunition of monetary policy. The critics of further quantitative easing measures also include the Executive Board members from Luxembourg, Austria, the Netherlands and Estonia.

Currently 1 USD = 0.80 Euro.

What is to stop them from making it look like 1 USD = 10 Euro? They won't do that of course. But who knows? The temptation to devalue against dollar will be there. It will immediately re capitalise the balance sheet of so called PIIGS. It will force people to look for alternative store of value to both dollar and euro!

-

panduranghari

- BRF Oldie

- Posts: 3781

- Joined: 11 Aug 2016 06:14

Re: Perspectives on the global economic changes

Seems like Cameron is talking about things to come

David Cameron warns of looming second global crash

David Cameron warns of looming second global crash

David Cameron has issued a stark message that “red warning lights are flashing on the dashboard of the global economy” in the same way as when the financial crash brought the world to its knees six years ago.

Writing in the Guardian at the close of the G20 summit in Brisbane, Cameron says there is now “a dangerous backdrop of instability and uncertainty” that presents a real risk to the UK recovery, adding that the eurozone slowdown is already having an impact on British exports and manufacturing.

His warning comes days after the Bank of England governor, Mark Carney, claimed a spectre of stagnation was haunting Europe. The International Monetary Fund managing director, Christine Lagarde, expressed fears in Brisbane that a diet of high debt, low growth and unemployment may yet become “the new normal in Europe”.

Cameron has adopted the more sombre tone in the runup to the chancellor’s autumn statement on 3 December, when the Office of Budget Responsibility will produce new growth forecasts and spell out the impact on public finances.

“The eurozone is teetering on the brink of a possible third recession, with high unemployment, falling growth and the real risk of falling prices too,” Cameron writes. “Emerging market economies which were the driver of growth in the early stages of the recovery are now slowing down. Despite the progress in Bali [trade talks in 2013], global trade talks have stalled while the epidemic of Ebola, conflict in the Middle East and Russia’s illegal actions in Ukraine are all adding a dangerous backdrop of instability and uncertainty.”

The emphasis on potential dangers, balancing some more hubristic ministerial accounts of the state of the UK economy, reflects Cameron’s concern – underlined by conversations at the G20 – about the extent to which Britain can detach itself from gathering economic storms.

Politically, Conservatives believe an emphasis on the risks still facing the UK will make anxious voters recoil from handing stewardship of a fragile economy to a relatively untried Labour team.

Some recent polling has seen the economy decline as an issue for voters, partly because there is a belief that the recovery is secured, leading to issues such as the health service and living standards, which have been seized upon by Labour, to rise in importance.

But with Germany, Europe’s manufacturing powerhouse, growing by just 0.1% in the third quarter, the eurozone economy appears to be faltering.

A European Central Bank (ECB) survey showed that inflation would remain at worryingly low levels before picking up slightly next year. The annual inflation rate in the eurozone was near a five-year low of 0.4% in October and the ECB expects a rate of 0.5% for 2014 – well below the target of close to 2%.

The EU may also be only one or two new rounds of sanctions away from pushing Russia into a deep recession as punishment for its interference in Ukraine, a point made in Brisbane by the Russian president, Vladimir Putin.

Cameron stresses that retreating from the world or imposing extra tax and borrowing may seem easy solutions but they would instead prove only to be a repeat of the mistakes of the past.

He claims that the G20 communique hammered out over the past few days endorsed Britain’s determination to use monetary policy to support growth and he would not waver on his policy of paying down government debt.

Re: Perspectives on the global economic changes

Real Conversations: Crisis Coming? Stockman on ‘Likely Global Recession’ & Consequences of the Fed

Re: Perspectives on the global economic changes

David Cameron seems Anxious about the Economy , How Nice of Him

Max Keiser and Stacy Herbert discuss David Cameron doubling down on failure as “global recession looms.” With a fair and balanced view at Cameron’s claims of “paying down government debt,” Max and Stacy concede that national debt growing from £580 billion in 2007 to £1,400 billion today could, using certain accounting tricks, be seen as the shrinking debt load. In the second half Max interviews Reggie Middleton of BoomBustBlog.com and Ultra-Coin.com about the block chain, the tech sector and more.

http://rt.com/shows/keiser-report/20693 ... ax-keiser/

Max Keiser and Stacy Herbert discuss David Cameron doubling down on failure as “global recession looms.” With a fair and balanced view at Cameron’s claims of “paying down government debt,” Max and Stacy concede that national debt growing from £580 billion in 2007 to £1,400 billion today could, using certain accounting tricks, be seen as the shrinking debt load. In the second half Max interviews Reggie Middleton of BoomBustBlog.com and Ultra-Coin.com about the block chain, the tech sector and more.

http://rt.com/shows/keiser-report/20693 ... ax-keiser/

Re: Perspectives on the global economic changes

Who’s Ready For $30 Crude Oil Price?

As to how low the oil prices can go, that depends on how much China will slow down as the number-one consumer of oil. China’s financial system is operating on record leverage at the moment. Record leverage in the financial system and a sharply weakening real-estate market suggest that their economic slowdown has the potential to carry far below Beijing’s GDP growth target of 7%.

Yes, China has had three real-estate downturns in the past seven years, but the latest one is coming at a time of debt-driven boom, which means the consequences this time can be quite different. I used to think that China was a classic savings-and-investment economic-growth model, and it was, but that was 10 years ago.

I no longer think that, since GDP growth in the past five years has come from ever-increasing leverage ratios in the banking system. No debt-driven boom is permanent by definition, so the decline in the Chinese real-estate market has the potential to create a domino effect there in 2015. If China does decelerate well below 7% in 2015, an oil price target in the $30 to $40 range is completely realistic.

I have to agree wit that conclusion. And I think China is doing far worse than it lets on. Even if official Beijing numbers fail to reflect this, the amount of oil imported should reflect it. recently, China, has stockpiled large quantities, but it has no limitless storage facilities. One would presume its demand on global oil markets may diminish quite a bit soon.

It’s interesting to see Martchev note that both the China economy and the US shale industry are extremely leveraged, i.e. both are in dangerously deep debt positions. The kind that a slowdown can hurt badly, if not murder outright.

Back in July, Wolf Richter pointed to the Ponzi that US shale has turned into:

[..] the Energy Department’s EIA has checked into it and after crunching some numbers found:

Based on data compiled from quarterly reports, for the year ending March 31, 2014, cash from operations for 127 major oil and natural gas companies totaled $568 billion, and major uses of cash totaled $677 billion, a difference of almost $110 billion.

To fill this $110 billion hole that they’d dug in just one year, these 127 oil and gas companies went out and increased their net debt by $106 billion. But that wasn’t enough. To raise more cash, they also sold $73 billion in assets. It left them with more cash (borrowed cash, that is) on the balance sheet than before, which pleased analysts, and it left them with a pile of additional debt and fewer assets to generate revenues with in order to service this debt.

It has been going on for years. During each of the last three years, the gap was over $100 billion.

If oil prices sink further on the lack of Chinese demand, perhaps even to $30-$40, what will be left of US shale? And I’m not even talking about the 75% or so output decline rates per well, which makes shale a questionable undertaking in the first place. I’ve said repeatedly that US shale is about money, not energy, that it’s a land speculation wager and not much else.

And even at $75 per barrel, that industry is already in big trouble. Not long ago, we saw indications that shale companies would keep drilling and producing full blast with their profit margins being strangled, out of fear that investors would walk away if they showed any sign of weakness. Now, that is no longer their biggest worry:

If China demand falls substantially in 2015, and prices move south of $70, $60 etc., that panic will be there. In US shale, in Venezuela, in Russia, and all across producing nations. Even if OPEC on November 27 decides on an output cut, there’s no guarantee members will stick to it. Let alone non-members.

And sure, yes, eventually production will sink so much that prices stop falling. But with all major economies in the doldrums, it may not hit a bottom until $40 or even lower. Oil was last- and briefly – at $40 exactly 6 years ago, but today is a very different situation.

All the stimulus, all $50 trillion or so globally, has been thrown into the fire, and look at where we are. There’s nothing left, and there won’t be another $50 trillion. Sure, stock markets set records. But who cares with oil at $40?

Calling for more QE, from Japan and/or Europe or even grandma Yellen, is either entirely useless or will work only to prop up stock markets for a very short time. Diminishing returns.

The one word that comes to mind here is bloodbath. Well, unless China miraculously recovers. But who believes in that?

Re: Perspectives on the global economic changes

Cross posting...

Looking back at the history

Looking back at the history

One book historians use to get great deal of insights into last 80 years of world finance, currencies, debt, gold is this book. If you have limited time, read first 40-50 pages.Have we considered currency exchange rates as a modern form of perpetuating slavery and transfer of resources?

Re: Perspectives on the global economic changes

http://www.soilandhealth.org/03sov/0303 ... ialism.pdf

Read the whole book online

Read the whole book online

Economic imperialism has produced some

weird and almost incomprehensible

results in its history, but never before has a bankrupt nation dared insist that its bankruptcy

become the foundation of world economic policy. But U.S. officials now insisted that

because of their nation’s bankruptcy on internat

ional account, all other nations must warp

their economies toward transferring its bankruptcy to themselves, stultifying their industries 226

and paying tribute to the beggar. Like the ITO before it, the GATT no longer served the

interests of the United States. As ITO was abor

ted, so the GATT was destroyed, whatever

the legal pretense of its status. The world body

whose functions had coincided with political

and economic realities in 1951 became a contradiction with the American reality of 1971.

The United States did not hesitate to reject it and to reassert its right to act unilaterally at all

times

Re: Perspectives on the global economic changes

Putin signs anti-offshore law to return Russian capital from foreign tax shelters

The law introduces amendments to the country’s tax code that will oblige Russian owners of companies registered in offshore tax havens to pay taxes in Russia.

The law stipulates a mechanism for taxation of undistributed profits of controlled foreign entities.

...........

Under the document, a Russian company or individual with ownership of more than 50% of a foreign organization in 2015 and with 25% such ownership from 2016 are categorized as “controlling entities.” The individual threshold will fall to 10%,

Re: Perspectives on the global economic changes

Does China view the U.S. as a failing economic power?

http://finance.yahoo.com/news/is-china- ... 54382.html

http://finance.yahoo.com/news/is-china- ... 54382.html

Still, America’s relationship with China is not all roses. In a recent editorial, Beijing-based and state-run Chinese newspaper, the Global Times called America, “too lazy to reform,” and said that President Obama was doing an “insipid” job. According to The Wall Street Journal’s Andrew Browne, China perceives the U.S. as a failing economy and world power, while the U.S. views China as a monster economy that is growing rapidly. If these exaggerated perceptions are seen as threatening, argues Browne, they could lead to widespread disagreement between the two countries and even a potential military conflict.The Chinese government has singled out a number of American businesses operating in Asia. Antitrust probes have been launched against Microsoft (MSFT) and Qualcomm (QCOM).“The Chinese have very ambivalent feelings regarding [America],” says Doctoroff.“But make no mistake,” he says, many Chinese citizens still want to come to America to study and work for American firms “because they offer impartial opportunity.”According to Doctoroff, America is viewed as an absolutist country in China. “They think that we have a monopoly on the truth and [they] disagree with that fundamentally. The Chinese are profound pragmatists and relativists. So when we start preaching about the global order we have to tone it down a little and bring it back into a pragmatic question of efficiency.”The U.S. and China are strategic competitors, says Doctoroff, there is hostility but also agreement—and as of late, more agreement than ever.

Re: Perspectives on the global economic changes

Post-Soviet trade bloc to embrace $3 trillion financial system

The Eurasian Economic Union credit institutions’ aggregate reserves stand at over $2 trillion while the EEU’s stock market is valued at over $1 trillion

KAZAN, November 28. /TASS/. The post-Soviet trade bloc based on the Customs Union of Russia, Belarus and Kazakhstan will embrace a financial system worth $3 trillion, board member of the Eurasian Economic Commission Timur Suleimanov said at a forum on Eurasian economic integration on Friday.

The Eurasian Economic Union (EEU) is a new integration association, which will start functioning from January 1, 2015 instead of the Eurasian Economic Community (EurAsEC), which officially ceased to exist on October 10.

About a thousand banks with a capital of $250 billion are operating on the territory of the EEU member states, Suleimanov said.

The credit institutions’ aggregate reserves stand at over $2 trillion while the EEU’s stock market is valued at over $1 trillion, he said.

EEU member states’ mutual investments grew by 14% in 2013 from the previous year to $1.9 billion, he said.

“The investment figure reflects the level of the countries’ mutual confidence,” Suleimanov said.

The EEU labor market is estimated at 170 million people and accounts for about 2.5% of the global GDP.

The Treaty on the establishment of the Eurasian Economic Union was signed by the presidents of Russia, Belarus and Kazakhstan on May 29, 2014 in Astana.

The agreement is the basic document defining the accords between Russia, Belarus and Kazakhstan for creating the Eurasian Economic Union for the free movement of goods, services, capital and workforce and conducting coordinated, agreed or common policies in key sectors of the economy, such as energy, industry, agriculture and transport.

The agreement stipulates the transition of Russia, Belarus and Kazakhstan to the next stage of integration after the Customs Union and the common economic space.

The document says that the union is open for accession by any state sharing the union’s goals and principles on the terms agreed by the member countries.

The EEU members are currently Russia, Belarus, Kazakhstan and Armenia. Kyrgyzstan is expected to join the union soon.

-

panduranghari

- BRF Oldie

- Posts: 3781

- Joined: 11 Aug 2016 06:14

Re: Perspectives on the global economic changes

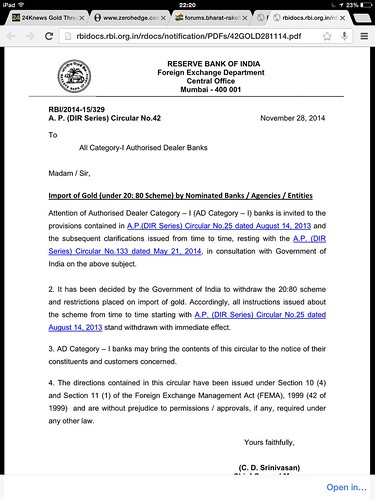

^^ What does it mean 20:80 gold import ?

Re: Perspectives on the global economic changes

Oil price drop may drive Europe back to Russian gas next year

* European utilities' long-term gas contracts oil-indexed

* Fall in crude could make these cheaper than spot gas

LONDON/MILAN, Nov 28 (Reuters) - Falling crude oil prices may boost European demand for oil-indexed gas next year, such as pipeline gas from Russia, when its price is likely to fall below spot prices.

Brent crude oil fell to an intraday four-year low of $71.12 a barrel on Friday, the day after OPEC decided not to cut supply, which dragged down other energy prices.

The drop in crude could make long-term gas supplies agreed between European utilities and Russia, Algeria and Norway cheaper thanks to their link to oil prices.

Utilities have spent years reducing their exposure to oil prices in their gas contracts by renegotiating deals and buying more gas on Europe's growing, freely traded spot market, which has been cheaper.

Now this trend may go into reverse.

"Spot prices could, in the future, become more expensive than oil-derived ones if oil prices were to drop significantly for an extended period of time," Societe Generale analyst Thierry Bros said.

Big shifts in oil prices take three to nine months to affect gas prices under long-term contracts, because adjustments are made based on the average oil price over a period of months.

"(A low oil price) may lead buyers to take cheaper long-term contract gas (from Russia) in larger amounts later in the winter, which would be bearish for prompt gas prices as and when these purchasing decisions hit the market," said Oliver Sanderson, an analyst at Thomson Reuters Point Carbon.

One analyst at a German energy company added that greater demand for Russian gas could hurt liquidity in some of Europe's spot gas trading markets.

Gas prices for delivery next year in Britain and its rival Dutch TTF hub were bearish on Friday, but spot prices regained some ground as they looked to immediate drivers such as consumption levels, temperatures and supply.

"There is a coupling between oil and gas prices, but it is more visible in futures and less in spot prices," Hans van Cleef, senior energy economist at ABN Amro, said.

"The effect of the oil price decline is not as much as the industry may fear. Oil prices are still above $100 a barrel on average for 2014, which is still pretty high."

Re: Perspectives on the global economic changes

Good Read on how the debt repayment thing works

Ponzi: Treasury Issues $1T in New Debt in 8 Weeks—To Pay Old Debt

Ponzi: Treasury Issues $1T in New Debt in 8 Weeks—To Pay Old Debt

-

panduranghari

- BRF Oldie

- Posts: 3781

- Joined: 11 Aug 2016 06:14

Re: Perspectives on the global economic changes

Of 100 kgs gold imported, 20 kgs should be re-exported overseas. It may be in the form of finished jewellery (thus making it a value addition increasing the export value) or to be sent back as gold coins or bars. India is perhaps the only big country without an official gold or silver coin. It is not really a bad thing. It just signifies the value to which Indians have held gold for millennia. The shape or the size or the name does not matter. what matters is the metal itself.Austin wrote:^^ What does it mean 20:80 gold import ?

Re: Perspectives on the global economic changes

Panduranghariji, I get the overall gold story. But this voracious appetite of Gold may have unintended consequences as explained in the following points. I'm not economist, so just the personal views...panduranghari wrote:Of 100 kgs gold imported, 20 kgs should be re-exported overseas. It may be in the form of finished jewellery (thus making it a value addition increasing the export value) or to be sent back as gold coins or bars. India is perhaps the only big country without an official gold or silver coin. It is not really a bad thing. It just signifies the value to which Indians have held gold for millennia. The shape or the size or the name does not matter. what matters is the metal itself.Austin wrote:^^ What does it mean 20:80 gold import ?

Some numbers first.

- India imported $58 billion worth of gold in the fiscal year ending March 31 2012, up from $38 billion in the previous fiscal.

- Together oil and gold imports make up an estimated 70 percent of the country’s trade deficit

- India’s household gold consumption has gone up from $19 billion in 2009 to $45 billion in 2011

- 50 percent in imports of gold and other precious metals in the first three quarters of this year (2011-2012)

Now the unintended consequences in my view (some influenced by publicly stated views of others)

If that $60 bn that we sent overseas to support foreign economies, were deployed at home creating road, infrastructure in the form of state/local debt which pays investment returns to its citizens, it can change the economy dramatically while creating tons of jobs.1. India is a net importer, and top international buyer of gold. When average Indian buys gold at the jewelry story, on a net basis, that gold was brought in from Africa or Australia or one of those gold exporters. Indians turn in their personal savings (Rupees) to someone who converts it into dollars from Indian Govt to buy gold from overseas. Govt loses its dollar reserves in exchange for a 10% import duties.

2. Demand of gold supports gold miners, producers, land owners, state and local governments "overseas". It creates jobs overseas, creates and supports mining and other earth moving large equipment producers, and also need for and use of newer technologies. The gold production overseas is in part funded by large debt market which support investment banks, stock markets. Every future cash flow is naturally levered, which again goes backing the banking system. None of this helps India, or Indians who are simple buyer of an end product.

3. Foreign Govts Taxation: All the gold production activities abroad are taxed at the corporate level. These taxes unlike in India, are systematically paid and distributed in those countries from country, state, and local municipality levels which further support local schools, hospitals, and infrastructure.

4. Paper Gold: Gold has led to the creation of modern "Paper Gold" and other variants in the stock market in the form of ETFs. Bulk of this financial paper is created and traded outside of India. India as one of the top buyer of gold indirectly supports "Paper Gold" by supporting the prices. Unfortunately, India does not benefit from all the paper gold transactions outside its boundaries.

5. In spite of being the top buyer of Gold, India can't enforce the use of Rupee as a currency of exchange. None of the commodities exchanges in India have any control over the pricing of the metal or its variants.

One a gold biscuit, bar, or jewelry is purchase, the story sadly ends there.

Re: Perspectives on the global economic changes

My view its about Paper Money verus Real Money .....IF we are importing Gold spending paper money in the long term this is good because Gold has been real money for thousand years...the paper money we see today will eventually melt down and something else may come up but if we have Gold it will put us in Good Standing long term along with our Growing Economy.

I just wished GOI actually imported more gold as reserves then the people

I just wished GOI actually imported more gold as reserves then the people

Re: Perspectives on the global economic changes

Didnt knew Brazil Economy was doing badly too

Brazil Recovers From Recession at Slower-Than-Forecast Pace

Brazil Recovers From Recession at Slower-Than-Forecast Pace

Re: Perspectives on the global economic changes

Chinese Stock market valued at $ 4,48Trillion

China Overtakes Japan as World’s Second-Biggest Stock Market

China Overtakes Japan as World’s Second-Biggest Stock Market

Re: Perspectives on the global economic changes

Its just as well that the people in India are importing and holding the gold rather than govt. History has shown time and time again that banking goons have conned and robbed govts store house of the peoples' gold through financial chicanery or when that failed.... warfare. Its harder to pry gold directly from the hands of the vast multitude because its so dispersed.Austin wrote:My view its about Paper Money verus Real Money .....IF we are importing Gold spending paper money in the long term this is good because Gold has been real money for thousand years...the paper money we see today will eventually melt down and something else may come up but if we have Gold it will put us in Good Standing long term along with our Growing Economy.

I just wished GOI actually imported more gold as reserves then the people

That's why its always better that the wealth be in the hands of the vast majority of peasantry rather than in some storehouse at the king's mansion just waiting to get robbed by banker con men.

The G-20 was definitely setup by the G-7 to coerce developing countries into backing the worthless fiat money standard and not to make claims on the global stock of gold. It will not last long and I predict when it comes crashing down, those promoting the unspoken agreement will be the first ones violating it - if they aren't already!

Re: Perspectives on the global economic changes

Come to think of it , US is not implementing IMF reforms which gives the BRICS nations specially the big one like China and India more say in the institution on some flimsy ground like blocked by Congress.Neshant wrote: The G-20 was definitely setup by the G-7 to coerce developing countries into backing the worthless fiat money standard and not to make claims on the global stock of gold. It will not last long and I predict when it comes crashing down, those promoting the unspoken agreement will be the first ones violating it - if they aren't already!

You can really expect the present institution like IMF to ever take a balanced view on Fast Growing Economies

Re: Perspectives on the global economic changes

Austinji (or anyone), would you please be able to give me some examples from last 3-4 centuries when holders (citizens or nation state) of real money , i.e. Gold, were "rewarded" for owning Gold, i.e. real money, compared to people/state who held other forms of money/currency (anything including fiat)? And, what I mean "rewarded" is that these people (i.e. holders of real money) RECEIVED or BECAME OWNERS OF large portion of scarce natural or other resource (non metal of course, once which are consumed), due to their "wisdom" and "courage" of owning real money. Thanks.Austin wrote:My view its about Paper Money verus Real Money .....IF we are importing Gold spending paper money in the long term this is good because Gold has been real money for thousand years...the paper money we see today will eventually melt down and something else may come up but if we have Gold it will put us in Good Standing long term along with our Growing Economy.

I just wished GOI actually imported more gold as reserves then the people

Re: Perspectives on the global economic changes

During industrialization, the global FREE powers switched to gold at the beginning. So those who could control some amount of Gold could trade and participate in the international industrialization. Rest of people were, including Indians, under colonial rule.

Re: Perspectives on the global economic changes

if the alternatives such as brick bank and AIIB were not raised and powerful enough, USA and EU would never accept China as one real decision~maker of WB or IMF. china now is telling USA that " Reform WB and IMF as I wish, otherwise I will replace them with BRIC bank and AIIB. BTW, until india were powerful enough to lead one powerful alternative to UN, P5 could never accept india as a new veto~holder of UNSC.Austin wrote:Come to think of it , US is not implementing IMF reforms which gives the BRICS nations specially the big one like China and India more say in the institution on some flimsy ground like blocked by Congress.Neshant wrote: The G-20 was definitely setup by the G-7 to coerce developing countries into backing the worthless fiat money standard and not to make claims on the global stock of gold. It will not last long and I predict when it comes crashing down, those promoting the unspoken agreement will be the first ones violating it - if they aren't already!

You can really expect the present institution like IMF to ever take a balanced view on Fast Growing Economies

Re: Perspectives on the global economic changes

Vishvakji, if I attempt not to precisely time the industrial revolution, it looks like it happened during 1750-1860. The esteemed FREE powers you are referring to here, had already started occupying, looting, and plundering Africa and Indian subcontinent centuries before 1700s. How can someone switch to Gold standard, acquired by looting, plundering, and claim that this is the new standard; thus the owners have the right to own more resources? It suggests that it had nothing to do Gold, but the collective enforcement of their will by Goondagardi on others. You are suggesting that those who could control gold, could trade. It is again another example of union Goondagardi, and it has little to do with Gold (thollar, euros etc.) isn't it? Today oil trades in thollar, not because the fiat currency is great. It is about enforcing ones will on others and using convenient tools (e.g. gold standard, thollar standard etc) to limit other's abilities.vishvak wrote:During industrialization, the global FREE powers switched to gold at the beginning. So those who could control some amount of Gold could trade and participate in the international industrialization. Rest of people were, including Indians, under colonial rule.

What it has anything to do with Indians being under colonial rule?

Last edited by chanakyaa on 01 Dec 2014 00:22, edited 1 time in total.

Re: Perspectives on the global economic changes

Swiss Say ‘No’ to Measure Forcing SNB to Acquire More Gold

From Swiss National Bank

Gold initiative

From Swiss National Bank

Gold initiative

On 20 March 2013, a popular initiative ‘Save our Swiss gold’ (gold initiative) was submitted. It demands that the SNB hold at least 20% of its assets in gold and that the central bank no longer be permitted to sell gold. In addition, it calls for mandatory storage of these gold reserves in Switzerland. In its message of 20 November 2013, the Federal Council recommended that the initiative be rejected. (why reject local storage requirement??) The SNB shares the view that acceptance of the initiative would have negative consequences both for the SNB’s monetary policy and for its investment policy.

Gold played a key role in the international currency order for a long time, but lost its function as the linchpin of this order when the Bretton-Woods system of fixed exchange rates collapsed in the years 1971–1973. Thereafter, the sole purpose of the Swiss franc statutory gold parity was to report gold holdings on the balance sheet. Finally, in 2000, with the revision of the Federal Constitution, the gold parity was formally abolished. In our present currency system, there is no direct link between the share of gold in the SNB balance sheet and price stability. Instead, price stability is ensured by the SNB as an independent institution that provides the economy with an appropriate supply of money and secures confidence in the stable value of the Swiss franc through a monetary policy geared to stability.

The 20% minimum share of gold in SNB assets called for in the initiative, together with the fact that the gold could not be sold, would have serious consequences for monetary policy. The SNB’s monetary policy has a direct impact on the size and composition of its balance sheet. Acceptance of the initiative would severely restrict the SNB’s monetary policy capacity to act. This would make it difficult for the SNB to conduct a monetary policy which ensures price stability and contributes to the stable development of the economy. Actions such as the minimum exchange rate against the euro or large-scale preventive measures to secure financial stability could no longer be announced and implemented with the same resoluteness. The latest crisis, in particular, has shown how important it is for the SNB to be able to expand its balance sheet flexibly when needed. In future, the SNB will also need this flexibility to reduce its balance sheet, as necessary. This flexibility would be severely impaired by the measures demanded in the initiative.