Todays edition of doom ***** presented by courtsey of Saxo Bank & Mish by me.

Link

Read the whole post. Its worth it. Some snippets.

End of a Cycle Like No Other - Steen Jakobsen - CIO

Please explain to me how a 35-year-old can be less optimistic about the future than a 55-year-old! It defies logic, nature, and reasoning. It is a case of young people feeling the pain of the present economic reality: it’s hard to find a decent job and or even interview for a job when you need a PhD to start with. The young are increasingly indebted by education costs and priced out of getting onto the house ownership ladder.

<snip>

Equity Burnout - Peter Garnry - Head of Equity Strategy

<snip>

Dollar is a Time Bomb and the Fuse is Burning Faster - John Hardy - Head of FX Strategy

When the Fed tightened policy starting in late 2013, the supply of printed US dollars started drying up and the USD exchange rate went increasingly vertical. Many forget just how bad a year 2015 actually was for global asset prices, particularly in emerging markets, and it was the lucky timing of the European Central Bank’s extreme QE starting in early 2015 and China’s eventual massive stimulus starting later that year that likely kept the world from dipping into recession.

But now, most of the policy punch bowls around the world have been removed or are nearly empty. China’s growth priorities are changing to priorities centred on the standard of living for everyone, as well as environmental policy, and Beijing also faces the onerous task of addressing its own credit bubble.

The Fed, meanwhile, continues to tighten policy and supposedly intends to shrink its balance sheet at an accelerating pace. Elsewhere, the ECB has promised to cease expanding its asset purchases entirely by late this year. Only the Bank of Japan continues to drag its heels, though it has also tapered its rate of asset purchases over the past year.

The removal of global policy stimulus has naturally come about as the world economy finally managed a couple of quarters of synchronised growth in 2017. But our view is that this growth is tenuous and very late-cycle, particularly in China and the US, as the credit cycle has already turned. And the next challenges for markets are just around the corner.

<snip>

Last September, the Bank for International Settlements estimated that there was a net $25 trillion in USD-denominated debts and derivatives in the offshore financial system. The world can ill afford another USD funding mishap, one that has already partially been set in motion by Trump’s corporate tax cuts, which are encouraging US corporations to repatriate hundreds of billions of USD from outside the US and draining liquidity from the offshore USD system.

<snip>

In a highly leveraged economy like the US, credit is a key determinant of growth. Lower credit generation is expected to translate into lower demand and lower private investment in the coming quarters. There is a high 0.70 correlation (out of one) between US credit impulse and private fixed investment and a significant 0.60 correlation between credit impulse and final domestic demand.

<snip>

These indicators suggest that the US is at the end of the business cycle – which is not much of a surprise – and hint that recession is just around the corner and Trump’s economic policy does not seem able to avert it.

Even unconventional indicators are sending warning signs. Product sales by paper and paperboard mills, which reflect the evolution of sales and therefore give a signal about the future evolution of production, have been falling since the beginning of the year. Although this indicator is certainly less reliable than in the past due to the digitalisation of the economy, there is still an obvious correlation with the economic cycle.

<snip>

US consumer confidence has returned to a high level but households’ financial situation remains gloomy. Household debt is at a new record of $13 trillion and the most fragile households are starting to face serious difficulties due to higher interest rates and tightening credit conditions.

Even though we agree that history does not always repeat itself, it is interesting to note that historically, such levels of consumer confidence have been followed by recession and a lost decade. This is too much of a coincidence, is it not?

Delinquencies have increased considerably over the past few months, especially in subprime auto loans where serious delinquencies have reached ‘Lehman moment’ proportions, as well as in credit cards.

<snip>

Commodities Go There Separate Ways - Ole Hanson - Head of Commodities Strategy

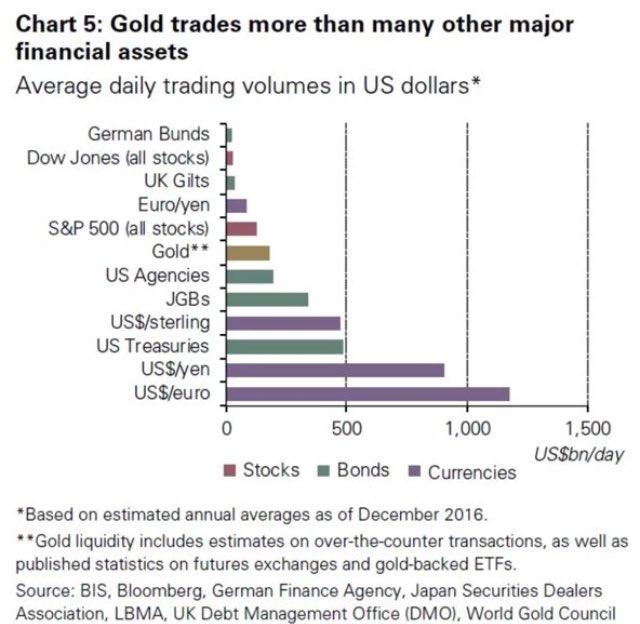

Gold is one of a few metals that has managed to hold onto a positive return this year. However, after several failed attempts to break through the $20 band of resistance above $1,355/oz, many investors have for now adopted a wait-and-see approach.