Re: PRC Economy - New Reflections : April 20 2015

Posted: 30 Aug 2017 15:49

Well No different then what Unkil to a great extent and EU to some extent does it ......Unkil would sanction any body at drop of pin

Consortium of Indian Defence Websites

https://forums.bharat-rakshak.com/

It is absolutely not the same thing. Western nations do this as a last resort, to 'rogue' nations that they have little ties with, like Iran or North Korea.Austin wrote:Well No different then what Unkil to a great extent and EU to some extent does it ......Unkil would sanction any body at drop of pin

Oh please spare these homilies , Western nation would sanction any one if they do not agree with their policy or try to go against it , International sanctions are applied ,bank account frozen and individiual sanction along with companies they have done worse sanctioned nation and killing lakhs of children in Iraq........what china has done is just mini-me of what the west has been doing for decades to other nations and still do it.Bart S wrote:It is absolutely not the same thing. Western nations do this as a last resort, to 'rogue' nations that they have little ties with, like Iran or North Korea.Austin wrote:Well No different then what Unkil to a great extent and EU to some extent does it ......Unkil would sanction any body at drop of pin

This is plain underhanded unfair trade practices, the equivalent of which would be the US sanctioning Mexico or Canada because they criticized Trump!

There is no reason for us to rationalize third-rate Chinese behavior and give them a fig leaf by drawing false equivalence with the West.

If China or Russia deployed ABM systems in Mexico or Canada, you can be your bottom dollar that they'll face American sanctions, and sanctions won't be the last resort either. Heck, Trump is threatening economic retaliations against Mexico for simply refusing to pay for a wall the Americans want to build.Bart S wrote:It is absolutely not the same thing. Western nations do this as a last resort, to 'rogue' nations that they have little ties with, like Iran or North Korea.Austin wrote:Well No different then what Unkil to a great extent and EU to some extent does it ......Unkil would sanction any body at drop of pin

This is plain underhanded unfair trade practices, the equivalent of which would be the US sanctioning Mexico or Canada because they criticized Trump!

There is no reason for us to rationalize third-rate Chinese behavior and give them a fig leaf by drawing false equivalence with the West.

The only western nation doing sanctioning is the US and then forcing its allies and friends to do the same. That said, the US won't sanction a major trading partner like China.Austin wrote: Oh please spare these homilies , Western nation would sanction any one if they do not agree with their policy or try to go against it , International sanctions are applied ,bank account frozen and individiual sanction along with companies they have done worse sanctioned nation and killing lakhs of children in Iraq........what china has done is just mini-me of what the west has been doing for decades to other nations and still do it.

That where US was smart compared to China. They finally made good with Cuba too. There will never be an ABM system deployed in Mexico or Canada against US. not for the forseeable future. compare that to countries around China- lets seeDavidD wrote:

If China or Russia deployed ABM systems in Mexico or Canada, you can be your bottom dollar that they'll face American sanctions, and sanctions won't be the last resort either. Heck, Trump is threatening economic retaliations against Mexico for simply refusing to pay for a wall the Americans want to build.

US is in far deeper economic shit hole then China and something they will never be able to come out and Mitchell Feierstein is to be believed the total debt is around $250 trillion if you count liabilities all the social entitlement program. Atleast china can still grow 3-4 % in worst , US has not grown beyond 2 % during entire 8 years of ObamaDavidD wrote:No, that's where the US is strong compared to China. Comprehensive national strength is really all that matters.

The Treasury Secretary echoed the words of the US envoy to the UN, Nikki Haley, by calling the fresh round of sanctions against Pyongyang “historic.” Mnuchin added “if China doesn’t follow these sanctions, we will put additional sanctions on them and prevent them from accessing the US and international dollar system.”

Washington has, so far, been reluctant to impose economic sanctions on China over concerns of possible retaliatory measures from Beijing and the potentially catastrophic consequences for the global economy.

Washington runs a $350 billion annual trade deficit with Beijing. China also holds $1 trillion in US debt, which amounts to 28 percent of US Treasury bills, notes and bonds held by a foreign government.

Trump chickened out on ROC when China insisted on one China policy or no talks with trump he relented.samirdiw wrote:Trump has to just supply nukes to ROC to give PRC a heart attack. Technically US can justify that it doesnt break NPT as it is still being supplied to China unless China insists that Taiwan is a separate country which it wont. Nothing else will work.

Full S&P text below.

People's Republic Of China Ratings Lowered To 'A+/A-1'; Outlook Stable

OVERVIEW

China's prolonged period of strong credit growth has increased its economic and financial risks.

We are therefore lowering our sovereign credit ratings on China to 'A+/A-1' from 'AA-/A-1+'.

The stable outlook reflects our view that China will maintain its robust economic performance and improved fiscal performance in the next three to four years.

RATING ACTION

On Sept. 21, 2017, S&P Global Ratings lowered the long-term sovereign credit ratings on China to 'A+' from 'AA-' and the short-term rating to 'A-1' from 'A-1+'. The outlook on the long-term rating is stable. We have also revised our transfer and convertibility risk assessment on China to 'A+' from 'AA-'.

The downgrade reflects our assessment that a prolonged period of strong credit growth has increased China's economic and financial risks. Since 2009, claims by depository institutions on the resident nongovernment sector have increased rapidly. The increases have often been above the rate of income growth. Although this credit growth had contributed to strong real GDP growth and higher asset prices, we believe it has also diminished financial stability to some extent.

The recent intensification of government efforts to rein in corporate leverage could stabilize the trend of financial risk in the medium term. However, we foresee that credit growth in the next two to three years will remain at levels that will increase financial risks gradually.

OUTLOOK

The stable outlook reflects our view that China will maintain robust economic performance over the next three to four years. We expect per capita real GDP growth to stay above 4% annually, even as public investment growth slows further. We also expect the stricter implementation of restrictions on subnational government off-budget borrowing to lead to a declining trend in the fiscal deficits, as measured by changes in general government debt in terms of GDP.

We may raise our ratings on China if credit growth slows significantly and is sustained well below the current rates while maintaining real GDP growth at healthy levels. In this scenario, we believe risks to financial stability and medium-term growth prospects will lessen to lift sovereign credit support.

A downgrade could ensue if we see a higher likelihood that China will ease its efforts to stem growing financial risk and allow credit growth to accelerate to support economic growth. We expect such a trend to weaken the Chinese economy's resilience to shocks, limit the government's policy options, and increase the likelihood of a sharper decline in the trend growth rate.

RATIONALE

The ratings on China reflect our view of the government's reform agenda, growth prospects, and strong external metrics. On the other hand, we weigh hese strengths against certain credit factors that are weaker than what is typical for similarly rated peers. For example, China has lower average income, less transparency, and a more restricted flow of information.

Institutional and economic profile: Reforms to budgetary framework and financial sector in progress

China's policymaking has helped it to maintain consistently strong economic performances since the late 1970s.

We project China's per capita GDP to rise to above US$10,000 by 2019, from a projected US$8,300 for 2017.

The Chinese government is taking steps to bolster its economic and fiscal resilience. We view the government's anti-corruption campaign as a significant move to improve governance at state agencies, local governments, and state-owned enterprises (SOEs). Over time, this could translate into greater confidence in the rule of law, improvements in the private-sector business environment, more efficient resource allocation, and a stronger social contract.

The government continues to make significant reforms to its budgetary framework and the financial sector. These changes could yield long-term benefits for China's economic development. The government also appears to be signaling that it will allow SOEs with lesser policy importance to exit the market either through merger, closure, or default in order to allocate resources more efficiently. More recently, it has also indicated financial stability as a top policy priority and is acting to rein in growth of public sector borrowing. However, we believe some local government financing vehicles, despite their diminishing importance, continue to fund public investment with borrowings that could require government resources to repay in the future.

China's policymaking has helped it to maintain consistently strong economic performances since the late 1970s. However, coordination issues between the line ministries and the State Council sometimes lead to unpredictable and abrupt policy implementation. The authorities also have yet to develop an effective communication channel with the market to convey policy intent, heightening financial volatility at times. Moreover, China does not benefit from the checks and balances usually coming from the free flow of information. These characteristics can lead to the misallocation of resources and foster discontent over time.

We expect China's economic growth to remain strong at close to 5.8% or more annually through at least 2020, corresponding to per capita real GDP growth of above 5.4% each year. We also expect credit growth in China to outpace that of nominal GDP over much of this period.

We project China's per capita GDP to rise to above US$10,000 by 2019, from a projected US$8,300 for 2017, given our assumptions about growth and the continued strength of the renminbi's real effective exchange rate. Over the next three years, we expect final consumption's contribution to economic growth to increase. However, we believe the gross domestic investment rate is likely to remain above 40% of GDP.

Flexibility and performance profile: External profile remains key strength

We expect financial assets held by the public and financial sectors to exceed total external debt by more than 90% of current account receipts (CAR) at the end of 2017. At the same time, we estimate China's total external assets will exceed its external liabilities by 65% of its CAR.

In 2017-2020, we project the increase in general government debt in each of these years at 2.8%-4.9% of GDP. We project net general government debt will fall toward 46% of GDP in the period to 2020 and interest cost to government revenue will remain below 5% throughout the forecast horizon.

We believe China's monetary policy is largely credible and effective. We believe the liberalization of deposit rates at banks in recent years is an important reform that could further improve monetary transmission in China.

China's external profile remains a key credit strength despite the recent decline of its foreign exchange reserves. We partly attribute the fall in reserves in 2016 to increased expectations of renminbi depreciation. Consequently, some private sector firms reduced or hedged their dollar debt and exporters kept a greater share of their proceeds in foreign exchange. We also attribute the accommodation of SOE and private-sector demand for foreign exchange as a willingness of officials to diversify China's external assets away from holdings of U.S. government debt to other investments of the financial and private sectors.

China remains a large external creditor. We expect financial assets held by the public and financial sectors to exceed total external debt by more than 90% of current account receipts (CAR) at the end of 2017. At the same time, we estimate that China's total external assets will exceed its external liabilities by 65% of its CAR. China's external liquidity position is equally robust. We expect the country to sustain its current account surplus at more than 2% of GDP in 2017-2020. We project annual gross external financing needs in 2017-2020 to total less than 60% of CAR plus usable reserves.

The increasing global use of the renminbi (RMB) also bolsters China's external financial resilience. According to the Bank for International Settlements' (BIS) "Triennial Central Bank Survey," published 2016, the renminbi was traded in 4% of foreign exchange transactions globally. We therefore assess the RMB as an actively traded currency. Demand for renminbi-denominated assets from both official and private-sector creditors could rise with the inclusion of the renminbi in the IMF's Special Drawing Rights basket of currencies.

We expect the share of renminbi-denominated official reserves to rise over time. If the renminbi achieves reserve currency status (which we define as more than 3% of aggregated allocated international foreign exchange reserves), it could strengthen external and monetary support for the sovereign ratings. Although the People's Bank of China (the central bank) does not operate a fully floating foreign exchange regime, it has allowed greater flexibility in the nominal exchange rate over the past decade. Based on estimates from the BIS, the real effective exchange rate has appreciated by close to 10% since the end of 2011. Any future weakness of the renminbi needs to be analyzed in this light.

China is gradually implementing an ambitious fiscal reform to improve fiscal transparency, budgetary planning and execution, and subnational debt management. These reforms could help the government to manage slower growth of fiscal revenue and lower its reliance on revenue from land sales.

In 2017-2020, we expect the Chinese government to keep the reported general government deficit close to, or below, 2.5% of GDP. However, off-balance-sheet borrowing could continue for the next two to three years. This reflects both the financing needs of public works started before 2015 as well as some new projects that the central government is willing to authorize to support growth. Consequently, we project the increase in general government debt in each of these years at 2.8%-4.9% of GDP.

We now include the entire sum of nearly RMB25 trillion (US$3.9 trillion, or approximately 36% of 2015 GDP) of government-related debt from local government financing vehicles in general government debt. We have also included the debts of China Railway Corp. in general government debt. The company was previously the Ministry of Rail but was incorporated as a special industrial enterprise. Bonds issued by the company are held on China banks' books at a lower capital charge compared with other corporate debt.

We offset these debts to compute net general government debt with fiscal deposits held by the government, net assets of the China Investment Corp. and net assets of the National Council of Social Security Funds. Using this method, we project net general government debt will fall toward 46% of GDP in the period to 2020 and interest cost to government revenue will remain below 5% throughout the forecast horizon. These forecasts in turn follow from our assumptions regarding real growth and ample domestic liquidity keeping financing cost low for the government.

Although the fiscalization of the local government financing vehicles and China Rail Corp. has raised our figure for general government debt, it has simultaneously decreased our estimates for contingent liabilities to the government from this sector. Entities with weak financial metrics owe much of the financing vehicle loans that are being redeemed through government bond issuance. By putting these loans on the government's balance sheet, the government has significantly reduced the banks' credit risks, in our view.

We believe China's monetary policy is largely credible and effective, as demonstrated by its track record of low inflation and its pursuit of financial sector reform. Consumer price index inflation is likely to remain below 3% annually over 2017-2020. Although the central government--through the State Council--has the final say in setting interest rates, we find that the central bank has significant operational independence, especially regarding open-market operations. These operations affect the economy through a largely responsive interbank market and a sizable and fast-expanding domestic bond market. The liberalization of deposit rates at banks in recent years is an important reform that could further improve monetary transmission in China.

Thank you Yensoyj and appreciate the detailed response. I can now see the rinse and repeat pattern clearly.yensoy wrote:Yeah and they can get investor visas for the money sunk into the fraudulent venture. Here's how it turns out:

1. Commit to invest 1M$; purchase land/building for about 200k, get a nice villa for 800k in company name - since this is a legitimate business proposition, Chinese government allows you to legally move your ill-gotten gains abroad (or you partner with a benami in Hong Kong - you will see how that works when you get to step eight)

2. Open shell company in HK. This is your distributor

3. Export junk from China to distributor (yourself) at market rate for this junk, probably $50k

4. Invoice junk for 250k and send it off to Canada; HK distributor now legally receives 250k from Canada; HK distributor sitting on 200k which belongs to you

5. Some of your inventory will sell, probably recover 100k from it as well after costs

6. Repeat steps 3, 4, 5 for some time; show that you have given jobs to xx number of Canadians for so many years

7. Get you investor visas/permanent residencies; meanwhile the little ones have been attending public schools at zero cost while you have been paying tax on tiny declared incomes

8. You also made a little money on the side besides getting your money back to HK for your sala to repeat the trick

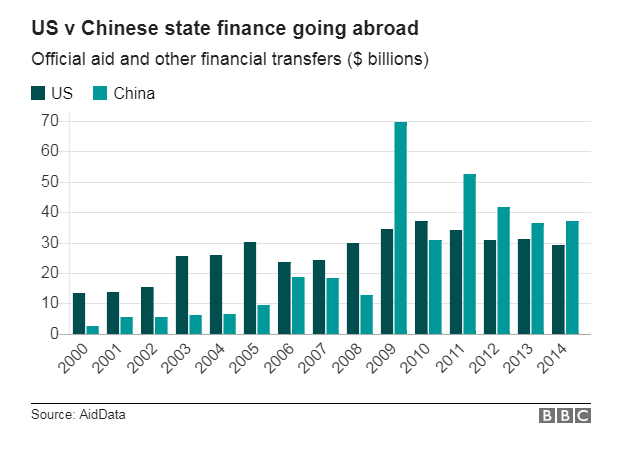

Not very long ago, China was a foreign aid recipient. Now, it rivals the United States as one of the world's largest donors, through traditional development aid or through financial loans.

For the first time, a large group of researchers outside China have compiled a major database detailing virtually all of China's financial money flow to recipient countries. Citing more than 5,000 projects found across 140 countries, it reveals that China and the US rival each other in terms of how much they offer to other countries.

However, "they spend those budgets in radically different ways. And the different compositions of those portfolios have far-reaching consequences", explains Brad Parks, the project's chief researcher

The vast majority (93%) of US financial aid fits under the traditional definition of aid that's agreed upon by all Western industrialised countries. That aid is given with the main goal of developing the economic development and welfare of recipient countries. At least a quarter of that money represents a direct grant, not a loan that needs to be repaid.

In contrast, only a small portion (21%) of the money that China gives to other countries can be considered as traditional aid. And the rest of that money? The "lion's share" of that money is given in commercial loans that have to be repaid to Beijing with interest.

"China wants to get attractive economic returns on its capital

For those interested in further details, recommend downloading and going through the original report belowUniversity of British Columbia studied how Chinese aid has changed countries in Africa, arguing that democratic reforms have slowed as the developing countries concluded they could bypass the political demands of Western donors by turning to Chinese aid.

"Traditional donors have criticised China's approach to aid," she says, but "many African countries embrace the assistance from Beijing, or at least are glad to have more options".

After years of trying, in recent months Beijing has finally made headway dealing with one of the most intractable problems facing the economy: reining in the rapid accumulation of corporate debt. Not only has the pace of the country’s debt build-up slowed significantly, but according to JP Morgan estimates, in the second quarter of this year the size of China’s outstanding stock of debt stopped increasing relative to the size of the economy, an important sign that the pace of debt accumulation has slowed to a sustainable level.

Beijing’s greatest success, however, is that it has managed to bring debt under control while maintaining robust economic growth. Deleveraging was widely expected to be a fairly painful process, resulting in an economic slowdown, and yet the Chinese economy is the most buoyant it’s been for years. However, the current success might be short-lived. Beijing’s deleveraging is being underwritten by government borrowing and inflation, two conditions that it may not be able to sustain for much longer.

The ordinary folks lost their savings and since then their Shanghai Index hasent grown much form the hay days of 5000 today it is around 3,300.nam wrote:They did loose 3 trillion in couple of months, however we don't know how much of that money went out of China as their stock market is not open to the world.

Their growth is backed by exception rise of Credits and NPA's , No one yet knows the consequences of this not withstanding the brave face the Chinese put up6.5 growth on a 12 trillion dollar, I won't call that slow. US wasn't growing at that rate when it was 12 trillion.

They are all in BIG BUBBLE Territory , It is just a question of when this pops and we will have a Tsunami effect probably much larger scale since 2008Chinese growth was always driven by printing money i.e bank loans. So is US through QE or Japanese gov printing money. As long as these gov can collect enough taxes.. it will continue. Ofcourse the side effect is inflation, with US being a higher valued currency can contain it better.

As I mentioned in my post, Chinese print money. They have always been in a bubble, since very long. People in India cry about increasing fiscal deficit from 3.5 to 3.7, the Chinese gov is at 15% ! They sustain because they manage to get some returns for this deficit, in form of exports.Austin wrote: They are all in BIG BUBBLE Territory , It is just a question of when this pops and we will have a Tsunami effect probably much larger scale since 2008

Yes you just listed the entire developed world.Austin wrote:Not just chinese the EU , US , Jap CB were printing money and still do that has made market grow exponentially now we are in 9th year since 2008 and the debt today is exponentially more higher then we had in 2008

So you rather have us on a model (or non-model) like that of Bolivia, South Africa or your_choice_of_turd_world?Austin wrote:Chola , You are simply assuming that a Debt Based Money Printing Model by China , EU , US and Jap are a sustainable one and even though the western economy grows by barely an average of 2 % they can keep printing the money in Glory and Keep Raising the Stock Prices higher and higher till perhaps the Kingdom Comes.

There is no sound economic principle in your statements.Austin wrote:You need a sound economy based on economic principle where debt is balanced by Growth , You cannot go into unlimited money printing and hope that it works , All these countries are doing is creating a fertile ground for hyperinflation in the future when bubble cracks and their bond and stock market collapses.

from Quantitative Easing. Supply is not an issue in most developed economies, demand is. Inflation is the last worry they have, let alone hyperinflation, inspite of increase in the money supply. There wasn't hyperinflation when the bubble cracked the last time, so why would there be one now ?If central banks increase the money supply too quickly, it can cause inflation. This happens when there is increased money but only a fixed amount of goods available for sale when the money supply increases.