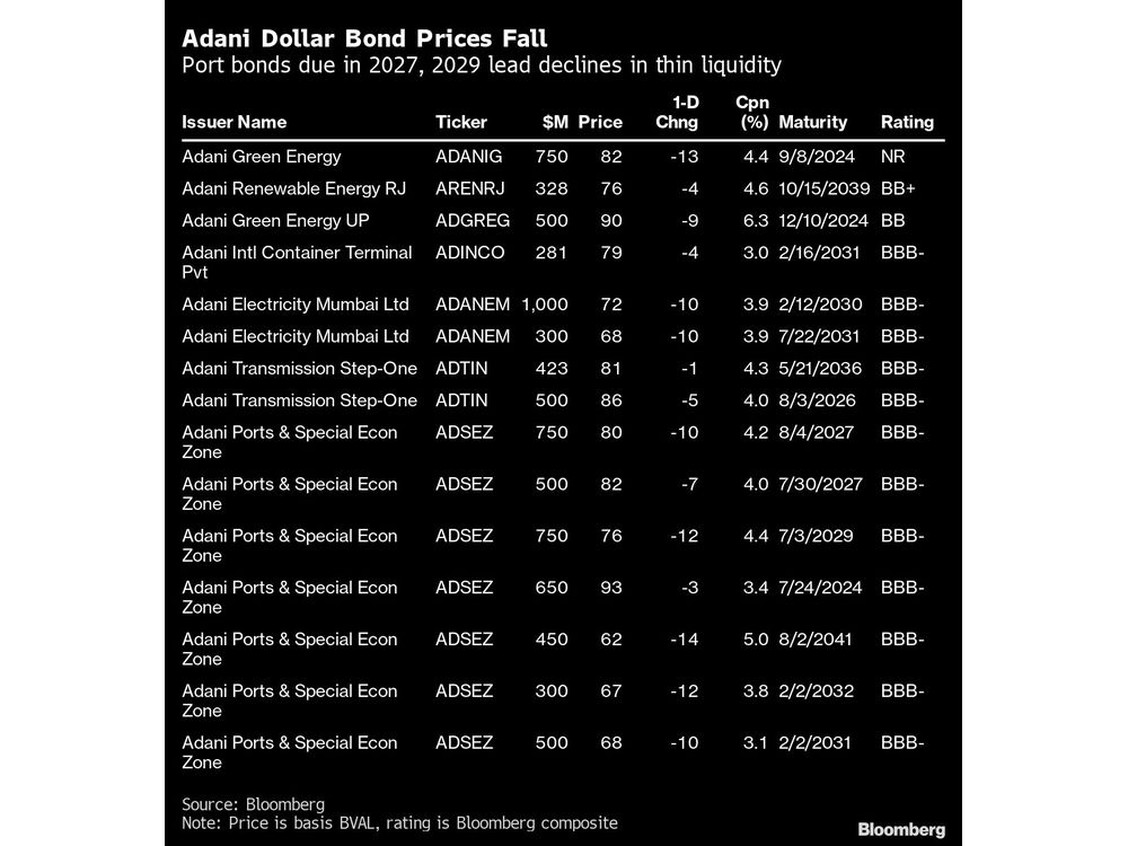

Reading the report, institutions refuse to lend additional capital (USD) to refinance maturing debt

This causes further panic if market realizes that company will not receive additional funds repay maturities. Remember, Adani earns majority of its earning in INR (not USD), which means it has to raise USD from somewhere.

Bond values drop and market realizes that company need to raise USD to repay debt

Hedge funds and fast money come in

If company can't raise enough debt to repay 2024 maturities, assets will need to be sold

How many of you will go ahead and invest in a company's bonds if it said in the prospectus "We expect to raise additional funds from the market to repay the principal when these bonds reach maturity" ?

Servicing debt ie paying interest and at the end the principal in USD while earnings are in INR adds an additional burden on expected financial performance.

1$ waz 70.4₹ in 2019, it's above 80₹ now. About 13% drop. So to pay the principal now in USD it will cost 13% more than the amount borrowed, on top of all the interest payments.

Annual inflation in india was about 5% approx.

So costs are up by nearly 30% over 5 years.

Underlying businesses are not solid - vulnerable to global economic slowdown and geopolitics.

Apparently their CFOs don't last very long, auditors are some garage firm, other auditors have put reservations. - see the H report.

Equity has tanked this week, unless Adani is able to refute every single allegation with factual data in a publicly held investors meeting and reassure every one, things look catastrophic for him and his group.

This "world's top X richest man" label will attract all kinds of media attention, some of it predatory. That's life.