1.

Writing to the Finance Member early in March 1937, the Governor stated that the situation was developing in a manner which required the serious consideration of Government. He pointed out that ‘the nationalist school of thought’ had its own suggestions to make for dealing with this problem. One suggestion (proposed to the Governor by Director Mr. B. M. Birla) was that the Bank should begin to buy gold. A second was to use the surplus for expansion, but the Governor did not favour it; he considered such a course inflationary! His solution was that Government should buy up their sterling debt, especially that maturing between 1948 and 1950. This he considered was ‘the most effective way of building up the financial independence of the country’.

2.

The only solution Sir James could think of, short of dropping the scheme entirely, was for the Bank to do the business as Government’s agent. As he confided to the Bank of England: the important thing is to get an early decision because in addition to other factors the passing of the Insurance Bill has led to a speculative rise in rupee gilt-edged with a consequent increase in the outflow of capital for investment in London. I am indifferent who gets the profits, or whether they are devoted to debt redemption or revenue, so long as I can get machinery into being to regulate these capital movements. I do not anticipate that I shall be able to do much but it seems to me that even a little is better than nothing. In India, also, the circumstances are not the same as in other countries. Elsewhere it might be arguable that it was immaterial whether external debt was redeemed through the central bank or directly by the investing public but in India it must be remembered that in many quarters the dogma that Indian exchange is too high and ought to be reduced by two pence has acquired an almost religious sanctity. Their devotion to this creed is not likely to be lessened if they stand a chance of gaining an additional 12 per cent by sending their money abroad.

3.

The scheme was, however, halted in February 1938, on account of the weakening of the exchange and the fall in the sterling purchases of the Reserve Bank. Apparently the Governor regarded this as a temporary phenomenon; in fact, he had taken some measures, especially the levering up of short-term money rates, to improve the exchange position. Therefore, he continued to press Government for acceptance, at least in principle, of his original proposal that the Bank do the whole business as a principal rather than as the Government’s agent, while still adhering to the principle laid down by the India Office regarding the appropriation of the ‘ profit ’ arising out of the transac- tions. His proposals, Sir James argued further, would give the Bank the necessary freedom of action to conduct the operations (viz., the purchase of the sterling stocks in the London market, passing them on to Government for cancellation, and sale of the rupee securities in the Indian market) at its discretion; besides, with its general reserve and also provident and similar funds to invest, the Bank could, without any embarrassment, hold much more paper than Government could, whereas under the existing procedure Government could easily be saddled with considerable quantities of rupee securities which was ‘neither sound in theory nor convenient in practice’. The Secretary of State was unconvinced by the Governor’s arguments. He found it difficult to accept the view that it was ‘sounder in theory or more convenient in practice’ that the rupee securities should be held by the Bank rather than by Government. According to him, it was hardly an opportune time to resume the repatriation operations owing to the uncertain outlook as regards the trade balance and the lower level of gold exports, not to speak of the uncertainty of world political and economic conditions in general.

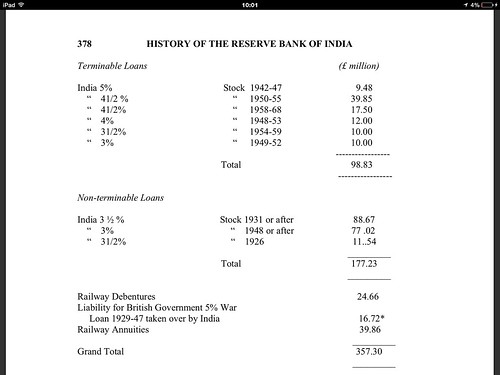

4.

After the outbreak of war, sterling began to accumulate with the Reserve Bank in substantial amounts and it appeared desirable to resume the Bank’s purchases in the London market for cancellation and issue of rupee securities there against. About the end of October 1939, India 31⁄2 per cent sterling Stock 1931 or after was quoted at about £79 1⁄2 against the quotation for the 31⁄2 per cent Rupee Paper in India of about Rs. 86-8-0; thus the purchase of sterling stock in London and the creation of rupee paper for sale to the public in India was a profitable proposition for Government. Operations were, therefore, resumed about the end of October and the first cancellation was put through on November 15, 1939. As a result of the operations, the disparity between the price of the 3 1⁄2 per cent India sterling Stock in London and the 31⁄2 per cent Rupee Paper in India was reduced and it soon became apparent that if repatriation was to be effected on a substantial scale a more comprehensive scheme would have to be introduced. The Bank’s external reserves had been built up to approximately 60 per cent of the note issue (excluding the hidden reserve in gold) and there was also a large sterling balance in the Banking Department; it was therefore felt safe to embark on repatriation on a larger scale.

5.

Simultaneously, an Acquisition of Securities Order was issued, transferring these securities to the U.K. Treasury, at the prices (the day’s quotations in London plus allowance for 2 1⁄2 per cent interest) notified in the Order. On the following day, i.e., February 8, a vesting order was issued by the Government of India under the Defence of India Rules, transferring these securities held in India to themselves at the prices notified in the U.K. Order converted into rupees at 1S. 6d. Owners in India were given the option to receive payment in cash (in rupees only) or in rupee counterpart securities. Unlike in the case of the Licence Scheme of February 1940 for conversion of the sterling loans into rupee counterparts which was administered by the Bank’s Bombay Office only, the facility was offered at both the Bombay and Calcutta Offices and no licence fee was charged; the object was to make the scheme as attractive as possible. Residents and rulers of Indian States fell outside the purview of both the British and Indian Orders; it was decided that these persons should be given the option, as were other residents of the sterling area outside India and Burma, to surrender their holdings to the Bank of England against sterling, and if they so desired, to the Reserve Bank against rupees or rupee counterparts. As agreed, the Government of India issued an Ordinance on February 8, 1941 deleting the proviso to Section 33(3) of the Reserve Bank of India Act. Two press communiques issued simultaneously explained the repatriation operation and the rationale of amendment of the Act. Neither the Central Board nor its Committee was formally consulted during the discussions leading up to the decision to requisition compulsorily the outstanding terminable sterling debt.

6.

The repatriation operation formed the subject of a very heated debate in the November 1941 session of the Legislative Assembly on a resolution moved by Mr. Jamnadas Mehta, recommending that’ in any fresh scheme of the repatriation of India’s sterling debt, care should be taken to see that the cost of such repatriation on India’s revenues is not unduly heavy as was the case with the last scheme ‘. The sting of the resolution was obviously in its tail! The mover charged Government with having incurred a loss of Rs. 35 crores on the whole transaction-Rs.15 crores (£ 11 million) in the discount allowed when the debt was incurred, Rs. 12 crores lost because advantage was not taken of the lower rate in 1939 and Rs. 8 crores lost because Government deliberately allowed the prices of the vested securities to rise by their open market purchases in London! There were other criticisms also against the operation and the rapid rate of accretion of the sterling balances. It was urged that the operation was undertaken more to help the British Government. A demand was made that the British Government should pay for their defence expenditure in India in rupees. The resolution was passed only after Mr. Mehta agreed to the deletion of the last few words referring to the cost of this operation as having been unduly high.

7.

The Governor also considered other possible alternatives to repatriation of the sterling debt. In his opinion, one course was to lend sterling, free of interest, to the British Government up to £100 million, to be repaid within a year or so after the war. Another (which actually came from the Finance Member) was to request the British Government to take over the non-terminable liabilities and pay them off as and when it suited them, since compulsory acquisition of the non-terminable loans, which Government were free to redeem on a year’s notice, might be the subject of still more unfavourable criticism in London business circles than in the case of the terminable stocks. Besides avoiding such criticism, the proposal had the theoretical justification that the liability in respect of India’s sterling loans would be shared to a certain extent by the British Government, a position which was recognised by the India Office as early as January 1930. While the first proposal appears to have been dropped at the Government of India’s level, the second expedient, which was put to the Bank of England by Sir James Taylor himself (and later to India Office by Government), was found unacceptable ‘partly because it would be most embarrassing to us as regards vesting by other Dominions and partly because of technical objections’.

8.

The Secretary of State was also opposed to the use, for repatriation, of sterling released by the revaluation of gold; the position would be very different, he added, if the proposition was to release gold in excess of Rs. 44.4 crores at the new valuation and sell it for dollars, in which case, the resultant sterling accumulation would fully qualify for treatment as’ surplus sterling’ in connection with repatriation proposals!

9.

The Government of India therefore urged the Secretary of State in the strongest possible terms to persuade the Treasury to agree to implementing the combined operation immediately. They cabled as follows on November 26, 1941: Opinion in India including Press is becoming increasingly critical of delay in effecting further stage of repatriation while prices continue to rise. In recent Assembly session resolution was passed that in any future scheme of repatriation care should be taken to see that cost was not unduly heavy. Debate was not without acrimony and charges were levelled that we were acting more in interests of foreign investor than of Indian tax naver. With a view to minimising ill effects of debate Resolution was accepted by Government in modified form omitting insinuation that last repatriation was unnecessarily expensive. Any material delay in respect of undated loans will put us in extremely embarrassing position. There is distinct possibility of Congress attending Budget session when fresh and still more virulent debate on repatriation must be expected. We regard it as most important that this should be avoided by fait accompli before beginning of session . . . . . In next Budget we shall have again to emphasise necessity of raising large rupee loans, main popular argument for which is repatriation, as means of financing war supply. If repatriation incomplete or capable of being represented as not having been carried out in manner reasonably favourable to India loan propaganda will suffer.

10.

On December 24, an order was issued by the Government of India transferring to themselves the holdings of these Stocks by residents in India at prices equivalent to those in the U.K. order converted into rupees at 1S. 6d

11.

The scheme contemplated an annual payment by the British Government of £6 million for 25 years tapering off gradually over the next 50 years, in return for a single capital payment by the Indian Government; the legal liability for the pensions was to continue to be that of the Indian Government.

12.

In a letter which Deputy Governor Deshmukh wrote to the Finance Department on January 14, 1943, the Bank’s objections to the Secretary of State’s views on the need for a high sterling cover were stated elaborately, and as it appears in retrospect so validly, thus: It is necessary to remind ourselves that whereas in 1934 when the rupee was statutorily linked to the sterling the latter was a dominating currency in international money markets and India was a debtor to Britain to a very large extent, today sterling is not in its old pre- eminent position and a reversal has already occurred of the debtor-creditor relationship between Britain and India, with the prospect of the process continuing at least as long as the war lasts. We believe that at the back of the public criticism of India’s growing sterling accretions and the concern expressed at their steady increase is the realization, whether it is expressed or implicit, that the international status of sterling is no longer what it used to be. It is this feeling that has obviously inspired the many non-official suggestions that in order to safeguard the solvency of its external assets India should endeavour to hold a larger proportion in either gold or dollars. Even from the historical point of view it is not so certain that theoretical opinion was unanimous that the principle of a percentage backing was suitable in all circumstances. There was the alternative theory that any such percentage should be subject to an overriding quantum limit in order that the size of the assets held in external currency should have some relation to the possible requirements of the country of that currency for correcting any temporary maladjustments. It could be argued, in other words, that some maximum limit, say, of £250 million, should be fixed for that proportion of external assets which is to be held in the form of sterling. Looking at the matter from another point of view, it will be easy to establish that the main demand on our sterling in the past has been for meeting the Home Charges on debt, pensionary and other establishment costs, and that neither the Currency Department nor its successor, Reserve Bank, has been called upon to sell exchange to anything like the same extent to make up shortages on private account. If that is so, then obviously with the almost spectacular diminution in the Home Charges that has taken place and is in progress the country need hold proportionately very much less sterling as part of its external assets against its foreign liabilities.

As regards the nature of India’s future foreign trade, it is not so certain either that in the post-war years it will run through channels requiring a large draught on its resources either in sterling or any other external assets. Very likely its internal trade will expand in the direction of making the country more and more self-contained, with the result that its requirements of external assets for the purposes of financing its foreign trade might not be on the scale which we were accustomed to see in the past. Thus from the point of view of the country’s probable future trade needs it could be argued that there was no case for increasing our present statutory requirements, but rather for lowering them. In spite of the virtual extinction of Home Charges that has already occurred or is imminent, we have, however, no intention of raising the question of the reduction of the statutory percentage under present circumstances. With the way sterling is accruing as part of the war effort, it does not appear to be a practical issue. If, however, the theore- tical question is raised of the desirability of our holding a larger percentage, we feel that we should set out the arguments to the contrary, particularly if our acquiescence was likely to be an impediment in finding sterling for any further funding operations that are regarded as otherwise fair and practicable.

12.

The postponement proposed in the date of capital payment disturbed Mr. Deshmukh (who had then assumed the Governor’s powers) considerably.

13.

The delay that had ensued between the Treasury’s first unofficial acceptance of the scheme in principle in February and the time when the India Office could put the proposals to it officially after the Viceroy’s Executive Council had given its approval had, in fact, hardened the attitude of the Treasury. The scheme was shelved indefinitely in February 1944 on the consideration that the proposals raised ‘fundamental problems affecting not only India’s balances but also the sterling obligations of the U.K. to other countries arising from the war’. It was only in July 1948, as part of the comprehensive agreement with the U.K. on the utilisation of the sterling balances, that the matter was finally solved through payment of £168 million for the purchase of annuities in respect of pensions payable to British nationals by the Government of India and the Provincial Governments,

14.

Although what had been accomplished so far in the matter of debt repatriation made an impressive showing, the sterling used for repatriation represented only about one-fourth of the sterling receipts of Rs. 1,649 crores from His Majesty’s Government from September 1939 to March 1946. There were, besides, substantial sterling purchases by the Bank in excess of the other commitments. Thus, the sterling balances of the Reserve Bank, which stood at the equivalent of Rs. 70 crores on the eve of the war, had risen to Rs. 1,724 crores at the end of March 1946. So, the problem of sterling utilisation was still there! The repatriation operations were summed up by the Finance Member in his speech on the budget for the year 1943-44, as follows: And thus India has completed the transition from a debtor to a creditor country and extinguished within the brief space of about three years accumulations over decades of its public indebtedness to the United Kingdom. Apart from the immediate exchange gain of a substantial relief from the necessity of finding sterling annually for the payment of interest charges, a great deal could be said on the implications of this remarkable change in India’s status. To deal adequately with that theme and to attempt to prognosticate the role which India is destined to play in the post-war world, would carry me far beyond the limits of a budget speech.